In this guest post, John Frame (former Bethanie and Baptistcare WA CFO) shares his views on the sustainability issues facing residential aged care providers with respect to how care is funded. He also points to potential solutions to help navigate an increasingly complex environment that is becoming more consumer-driven.

Residential aged care in Australia is complex, some may well argue far too complex, making it difficult to navigate as a care recipient, problematic as a provider of services and on a trajectory that some may suggest can well make it moribund in its present configuration.

It certainly is not recommended to look at the more recent Stewart Brown report before bedtime which shows the following for the residential aged care sector:

| $ per bed per day | EBITDA | Operating Result |

| June 2022 | $5.87 | ($14.67) |

| September 2022 | $0.13 | ($21.29) |

There are some fundamental flaws in the structure of aged care that strike at the very essence of the present issues facing the residential aged care (RAC) sector. There is however certainly an Elephant in The Room.

With the Federal Government recognising that with the Baby Boomers entering retirement and coupled with the advances in medications and treatments for chronic conditions and physical ailments, there will be an increasing demand for aged care services to support them to live at home. The consequential burden on taxpayer-funded care costs under existing funding paradigms will become massive and the call to pass some of that burden onto co-payments and co-contributions from recipients and changes to means-testing to include the family home has often been tabled.

This is confirmed in three reviews in the past two decades on the aged care system in Australia. The Hogan Report, The Productivity Commission Report, and the Tune Report, which each advocated significant similar-themed changes to the operating and financing systems in aged care, yet none were wholeheartedly embraced by most stakeholders.

Finally, a Royal Commission brought acute focus on some key aspects of the delivery of care and services requiring urgent attention in the aged care systems. The jury is out as to whether any real sustainable and meaningful outcomes will arise for the primary benefit of the care recipient and Providers who deliver the services.

The RAC sector has been asking the Federal Government for ever greater levels of funding to pay for care costs as an ongoing theme for as long as I can recall. Practically this means either taking taxpayer funding away from other essential services or increasing taxes to meet that extra cost. Therefore, the two questions that should be asked are:

- Will the Millennials, who soon will have a significant influence on the electoral vote be that keen to pay ever-increasing taxes to fund baby boomer care expenses particularly when the same baby boomers currently hold the bulk of assets?

- Where will the cuts be made in the Federal Government budget to redirect paying the huge increase in care costs? Should this come from Social Security, Health, Education, and Defence…?

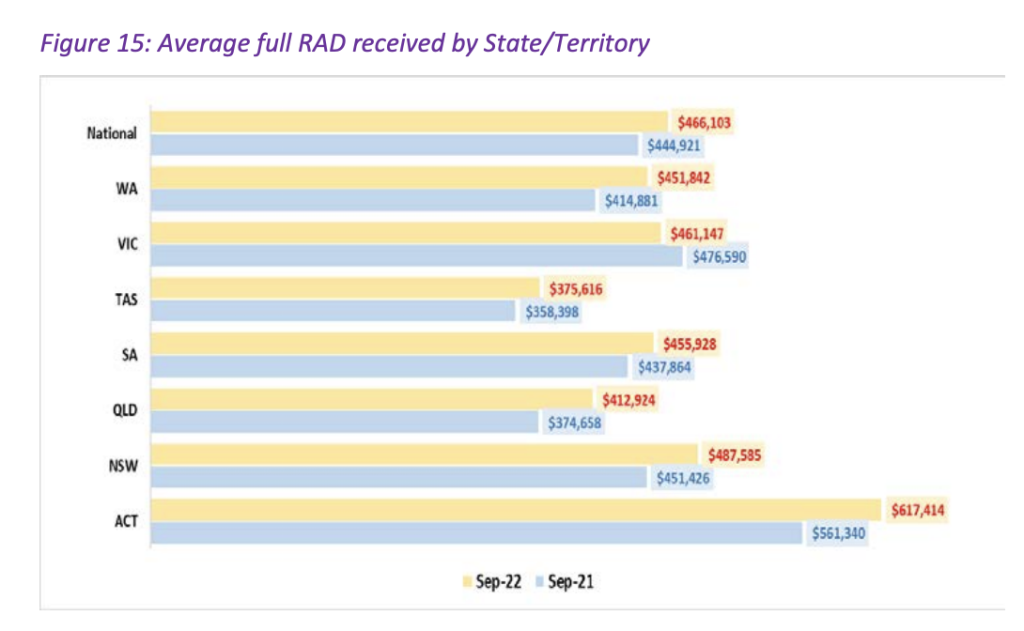

This brings me to the Elephant in The Room, that being the fundamental flaw that I see lies within the current and past RAC funding regime enabling circa $35 billion of debt, called Refundable Accommodation Deposit (RAD), which is real debt owed by Providers to residents, to be incubated for inheritance.

It’s a huge amount of capital lent by in-coming care recipient residents to RAC Providers as interest-free deposits to be repaid in full as that resident departs the facility; paid in practice to the Estate of the resident for the inheritance of that resident’s beneficiaries under the Will – leaving the taxpayers to pay for the costs of care services.

The early logic decades ago in setting up the RAD (Accommodation Bonds) system was to facilitate the construction of nursing homes by providers to meet growing demand.

Even many decades ago the cost-benefit analysis did not necessarily encourage investment into nursing home infrastructure, but with the Accommodation Bond system, it allowed business models to evolve whereby Providers could borrow construction funding from banks via interest-bearing loans that were soon repaid with in-coming non-interest-bearing resident RAD debt. The banks’ risk exposures were substantially reduced as the debt repayment risk passed relatively quickly upon a RAC completion to the Provider opening their doors to lend money to Providers. The business models of RAC Providers extended to repaying a RAD to an exiting resident, or their executor, from a RAD – paid as a new incoming resident replaces the space vacated by the resident leaving.

A key point is that RAD is debt that has to be repaid at some point and this sector owes residents, or rather their inheritance beneficiaries, a huge sum of money that is largely under-provisioned by Providers for repayment.

The RADs facilitated the construction of the large nursing home infrastructure across Australia, infrastructure that the EBITDA and Net-Results across the sector reveal is producing insufficient returns to remain sustainable or repay the RAD debts.

The Federal Government then further facilitated this arrangement by standing as guarantor for any RAD that was not paid back due to a Provider defaulting on the proviso it had recourse pari passu to collect the loss incurred from other RAC providers. The Federal Government has stepped in on occasions to repay defaulting RAD payments. It warrants consideration as to what could occur if a big provider default and the Government exercises its rights to collect the default amount from other Providers. That scenario has not yet occurred, but it inevitably leads to a domino effect on other providers.

The policy again changed to limit the purposes for which Accommodation Bonds may be used, effectively removing the retention amounts and disallowing the use of RADs to fund the cost of delivery of services. This effectively made RADs the lump sum future inheritance bond they are today, where the only effective use of the funds was to either repay debt for building more facilities or buy more land to build new facilities.

As a result and disturbingly the cash flow of many RAC Providers have been and still are such that they use the RAD to fund expansion and debt and do not make appropriate provision to repay their RAD debt, rather relying on the in-coming RAD to pay out-going RAD’s. However as care recipients choose to stay at home longer and therefore spend a shorter time in the nursing home and many elect to pay a Daily Accommodation Payment (DAP), as opposed to a RAD, some Providers have found that while a DAP is useful in assisting operational cash flow, any material net RAD outflow (that being repayment of the organisation’s debt) poses another level of stress in managing overall liquidity.

If anyone thinks that the workings of RADs in the RAC sector have elements of a never-ending cycle of waiting for ‘Peter to pay Paul’ they are perhaps not far wrong in wondering.

In mid-2024 a seismic paradigm shift is about to occur in the RAC sector when bed licenses; previously given free to RAC Providers – each license attaching a guaranteed annuity of income payable to the Provider – cease and a consumer-directed regime descends giving control of funding and choice of service provision to the care recipient and no longer with the Provider. For Providers who do not proactively re-engineer their operating processes and procedures and shore up their finances, we will likely witness even more nursing home organisations merging or exiting, hopefully without defaulting on resident debt repayments.

In essence, this RAD funding regime coupled with a lack of co-contribution or co-payments from recipients who can afford to pay, effectively means that we will see care recipients’ access taxpayer-funded care exponentially increase as the Baby Boomers continue to flow into the system, while their wealth is preserved for inheritance rather than contributing for their care. Where else in the world does this occur?

Additionally, we should observe the following funding scenario to assess if the system is working equitably.

Care recipient A:

Care Recipient: Pays a DAP based upon a RAD equivalent of $550,000 which is calculated at 7.06% pa = $38,830 pa.

Provider: A DAP directly assists a Provider operating cash flow as it effectively is the equivalent of a daily rental of $106.38 paid to occupy a bed in the RAC.

Care recipient B:

Care Recipient: Pays a RAD of $550,000. Earns no interest but is repaid in full on leaving the RAC.

Provider: The Provider may use the RAD to repay interest-bearing debt, thereby reducing its cost of borrowing when building a new RAC or refurbishing an older RAC which will assist in reducing capital cash outflow.

Let’s assume that the bank interest rate is 5.5% (circa 3% until recently). This ‘saves’ the Provider $30,250 pa (equates to $82.88 per day).

If the RAD is placed on deposit by the Provider say at 3.5% (was as low as 0.5%) this will earn the Provider $19,250 pa or $52.74 per day.

Care Recipient B is saving the Provider $30,250 pa in interest if the RAD is used to pay down interest-bearing debt on infrastructure or is earning the Provider $19,250 pa if the RAD is placed on deposit. Both amounts can be equated to a ‘rental’ paid by the care recipient to occupy the bed.

Table: Annual RAD / DAP contribution to Provider

| Care Recipient | A | B | C |

| $ selection | DAP | RAD – repay debt | RAD – on deposit |

| $550,000 RAD | |||

| Cash flow for Provider | $38,830 | $30,250 | $19,250 |

| The deficit in cash flow of RAD to DAP | ($8,580) | ($19,580) | |

| Rental Charge /day – DAP | $106.38 | ||

| Equivalent Rental Charge/day RAC | $82.88 | $52.74 |

A potential solution to fix both the anomaly between the DAP and RAD noted above and mitigate some of the cash flow pressures on RAC Providers would be to charge all care recipients a rental charge.

Care recipients who elect to pay a DAP are already paying a rental.

The rental charge payable by those care recipients who elect a RAD would be based upon the equivalent of a DAP, less the ‘deemed’ cash benefit to a Provider from the RAD. Just as the Government set a statutory DAP rate (Maximum Permissible Interest Rate – MPIR), a ‘deemed’ statutory rate would be attached to the RAD and a care recipient would have that rate differential deducted from the RAD upon leaving the RAC. In effect a retention sum that was in fact in place before the reforms that removed the specific right for a provider to hold a retention sum.

In the example above, if the ‘deemed’ rate is set at 5.5%, a care recipient who elects to pay $550,000 RAD would be charged an annual rental of $8,580 pa to be deducted from the RAD upon departure. (Calculation – 7.06% DAP MPIR less 5.5% deemed rate = 1.56% on $550,000).

Rather than asking should the Federal Government write a blank cheque to meet the tsunami of care costs barreling down with the baby boomer cohort, the paradigm shift question to be asked initially should be – ‘Is this RAD funding regime right or even equitable?’ Is it in fact appropriate that it be preserved intact as an inheritance for beneficiaries and not used to fund the actual cost of delivery of care and services?

John if only more aged care executives thought like you, and analysed the data as you do, perhaps we would have a sustainable model. Great article.